Goods and Services Tax

GST is a broad-based tax on domestic consumption.

Last updated 2 March 2026

What is GST?

Introduced in 1994, the Goods and Services Tax (GST) is a broad-based tax on domestic consumption.

How does GST work?

GST is collected by GST-registered businesses that act as collection agents on behalf of the Government.

GST is levied on:

Goods and services purchased locally from GST-registered entities; and

Goods and services imported into Singapore.

How has GST changed over the years?

When GST was introduced on 1 April 1994, the rate was 3%. This increased to 4% in 2003, 5% in 2004, 7% in 2007, 8% in 2023 and 9% in 2024.

Are some goods and services exempt from GST?

Yes. GST is not levied on certain goods and services:

Exempt items: the sale and lease of residential properties, provision of financial services, import and local supply of investment precious metals, and supply of digital payment tokens (e.g. cryptocurrencies) from 1 January 2020

Out-of-scope items: sale of goods that are not brought into Singapore and sales of overseas goods made within the Free Trade Zone and Zero GST Warehouses.

💡 Please refer to IRAS' website to learn more about GST exemptions.

Why don't we exempt basic necessities from GST?

This may sound attractive, but in practice:

Benefits mainly go to the more well-to-do: Wealthier households spend more on everything, including basic necessities.

Complex exemptions list creates loopholes: Having multiple rates creates confusing product distinctions and encourages businesses to game the system by getting creative so that their products are classified in lower tax tiers. This makes the system onerous to implement, unnecessarily complicating our GST system and increasing businesses’ compliance costs. Such costs may eventually be passed on to consumers.

Examples of disputes in other jurisdictions with multi-tier systems include whether mozzarella pizza toppings should be classified as “cheese” (and charged at a lower GST rate) depending on its vegetable oil content.

Instead, in Singapore, we designed a fairer and more effective system, tiered by income, such that lower-income households pay a much lower effective GST rate than higher-income households:

The permanent GST Voucher scheme to help lower- and middle-income households with their expenses.

The Government absorbs GST on publicly subsidised education and healthcare.

Why did Singapore raise GST to 9%?

Singapore’s needs are growing and evolving:

Healthcare

By 2030, around 1 in 4 Singaporeans will be aged 65 or above, up from 1 in 6 in 2024. We will need to spend more on healthcare to support our seniors.

Families and children

Accessible and quality childcare and early childhood education to give our children a good start in life and provide parents with better support.

Security

The range of threats we face is also wider, ranging from terrorism to cyber-attacks. We need to invest more in security to keep Singaporeans safe.

These are recurrent needs which must be funded with a recurrent source of revenue. Raising GST was the prudent and sustainable way to achieve this.

How is the Government helping Singaporeans to manage the cost of living?

Permanent support

Subsidies on education, healthcare, housing, and other assistance. GST absorption on publicly subsidised education and healthcare.

Permanent GST Voucher scheme

Permanent, targeted support for lower- and middle-income households, comprising cash, MediSave top-ups, U-Save and S&CC Rebate.

Assurance Package (AP)

Ensures that majority of the households do not feel the impact of the 2023/24 GST rate increase for at least 5 years.

Enhancements to AP (2022-2025)

Additional cash payments, U-Save, S&CC Rebate, and CDC Vouchers.

💡 Check what support you and your households qualify for with the Support for You Calculator.

Infographics

.png)

Assurance for 2025 Support for Singaporeans

Why did Singapore raise GST in 2023 and 2024

Why don't we borrow more instead of raising GST

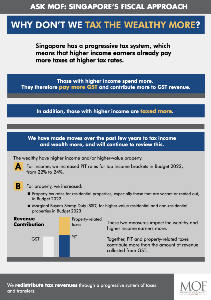

Why don't we tax the wealthy more